For the last year and half, I’ve fielded about a hundred different inquiries about The Athletic’s prospects for success in this media climate. The questions have come a little more than once a week via text, DM, email, on the phone and in person, and span a wide spectrum of both personal and professional contacts. I got the sense that most of the curiosity is looking to confirm their own skepticism about The Athletic’s future.

So you may be wondering two things at this point:

1) Why do these people care about what you think?

2) What did you tell them?

Answering the first question, many years ago I wrote at length about sports media startups like Bleacher Report, SB Nation, 24/7, Citizen Sports (not really a media company) and Yardbarker (where I worked for a while). I focused on the financial mechanics and the implications of what their investment rounds, partnerships, executive moves, and public analytics said about these companies in an effort to paint a comprehensive picture of what was happening behind the scenes.

As for the second, my answer was more or less something like, “They are going to need to raise a round of money at some point in 2018. Whatever shakes out there will tell us the trajectory they are on.”

** After you’re done here, please check out my interview with The Athletic COO Adam Hansmann about what’s next for the company.

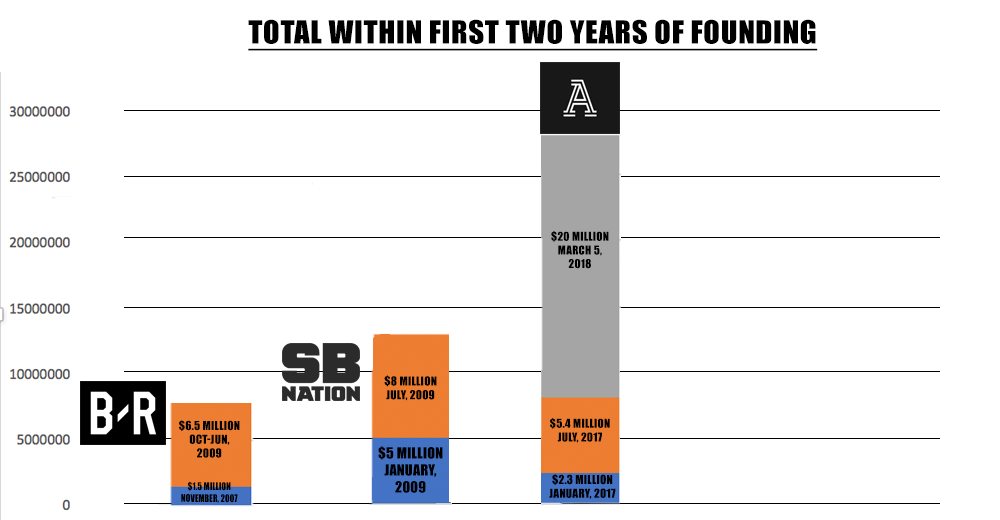

What $20 million in funding tells us

The $20 million most recently raised by The Athletic really blew my mind. In a previous article, we more or less explained that, historically, this is a VERY large round of funding, especially for a very young company. If you’re unfamiliar with venture capital, the basic premise is as follows:

** A company usually gets off the ground by either just putting in sweat equity early or taking a small round of money from friends and family. This is often an undisclosed amount. Crunchbase shows The Athletic raising some funds in September 2016, which is when the company graduated from Y Combinator, a prestigious startup incubator.

** The Athletic then raised a bit over $2 million dollars in January 2017. They termed this a “seed” round, which is usually a term used for rounds a bit smaller in size. But a lot of companies like to term early rounds as seed rounds, regardless of size. The Athletic then raised $5 million in funding this past summer which was their formal series A round. This latest round of $20 million (their series B) brings their total known funding to close to $30 million.

What’s impressive about The Athletic is that they raised three rounds of funding in less than 18 months. Most startups on the Silicon Valley fast track usually raise a round every 12 to 24 months because it’s a pretty daunting process. This signals that a) there was internal confidence the company could go out and raise funding, which is no layup and b) The Athletic had traction with investors and didn’t have to spend an excessive amount of time bringing in capital, which often can be a three-to-six-month process where a myriad of things can go wrong.

But it’s not just how fast The Athletic raised money; it’s more about how much money they raised. You will typically see each round of investment into a company increase, which typically mirrors an increase to the company’s valuation. Basically, the cost to get a piece of a growing company should always be going up.

Usually when funding events occur, info will leak out about how much the value of a company is judged to be. (The Athletic has avoided sharing anything here.) If you had asked me what I expected for The Athletic in a 2018 funding event, I would have guessed maybe an April-June round of $8 million to $12 million. Let’s say a $10 million dollar round (half of what they ended up raising) would give them a ballpark valuation of $30 million to $50 million (pre-money, meaning the value of the company before the additional funds were added to the company).

The Athletic raising $20 million, and so quickly, indicates that the company is valued in the $60 million to $100 million neighborhood (pre-money), which would be significantly higher than what other digital media companies were valued at during this stage. To put this into context, Bleacher Report sold for $175 million after a much longer five years of existence. Rivals (also a subscription model network) sold to Yahoo for $100 million in 2007 after a decade. To think that The Athletic is already at, close to, or over a nine-figure post-money valuation (counting its latest investment round) in under two years is not only startlingly impressive, but it requires recalibrating the traditional floors and ceilings of outcomes that observers believed a sports media startup could achieve.

Ultimately, whatever information The Athletic shared with investors inspired a lot of confidence for the company’s potential growth going forward. These are some of the factors that could compel resetting expectations for a sports digital media startup.

Revenue Certainty

The biggest thing going for The Athletic is the business model, one that doesn’t chiefly rely on advertising rates and page views. Using Awful Announcing as an example, I really have no idea how much this site will make next month. I could be more than 20% off in either direction guessing the traffic we will get. Likewise, I can’t really tell you the ad rates we’ll bring in for that traffic.

Facebook and Google can and have changed their algorithms, new ad blockers could be released on more browsers and platforms, display ad rates could spike or crater, and hell, it could just be a slow month. That’s the grind for most digital publishers and it’s why you’re seeing a lot of jobs disappear.

But The Athletic and other subscription sites are bypassing all that dreck. Guessing the number of new subscribers and the amount of cancellations is a much easier model to project and track. It’s not exactly a secret that we as consumers often maintain subscriptions either unknowingly or unwillingly due to laziness, busyness, or lack of awareness.

As we speak, there are millions of people still paying for dial-up internet who don’t even use it and haven’t in years. I still pay for a stupid Efax account (which costs more than a subscription to The Athletic and Netflix combined) and nobody has sent me a damn fax in maybe two years and yet that baby will auto-renew without me doing anything.

This is a long way of saying, The Athletic and any other business that have your credit card info and can auto-renew your subscription is a MUCH better business than relying on a myriad of other factors to drive revenue. Sure, other outlets can get you to follow, like, and sign up for notifications and emails, but ultimately if you don’t click onto their site or have an ad blocker on or ad sales just have a bad month, it’s just not going to help the bottom line.

No real competition

But wait, Ben! Haven’t subscription sports sites been done before? This isn’t really “new!”

Yes, a long, long, long, long time ago. Back in the late-90s, Rivals was launched and raised millions and millions of dollars going down this path. A failed IPO and a dot com crash reset expectations for them and Yahoo ended up acquiring it for a hefty $100 million in 2007 — which was a solid outcome, but one that didn’t live up to early expectations.

So what happened? Competition.

After Rivals was bought out of bankruptcy in 2000, the company’s founder Jim Heckman founded Scout, which was an exact replica of Rivals. What unfolded was years of lawsuits and turf wars over talent, publishers, TV deals, partnerships and, most importantly, subscribers.

The two sites not only split the market, but they burned through all of their cash trying to best each other. It didn’t end when Rivals sold to Yahoo and Scout sold to Fox, while 24/7 launched and further split the market. Only recently has this industry really hit a healthy place with Scout and 24/7 recently merging under the banner of CBS, but even that is a long, long story.

All three of these companies realized they had a good business model, but the competition among them nearly suffocated each operation at many points in time. By all accounts, Rivals and 24/7 are healthy businesses and have been for quite a while, but I’m sure anyone familiar with these companies would tell you it would be a whole different situation if the college recruiting network model was not engulfed by a decade and a half of costly turf wars.

Owned and operated under one consistent brand umbrella

While we’re talking Scout, Rivals, and 24/7, let’s also introduce the fact that these companies mostly relied on an affiliate business model. Using my alma mater (Ohio State) as an example, up until the Scout merger with 24|7, the following subscription sites existed:

- Buckeye Sports Bulletin (Scout)

- Buckeye Grove (Rivals)

- Bucknuts (24/7)

Neither of the sites’ branding includes the parent company prominently and these affiliate sites would often flip between networks like LeBron in free agency. In most cases, these local sites were not owned and operated by the network; they belonged to and were just affiliates with partnership deals in place. Non-subscription networks like SB Nation and Fansided made it a point to own the sites under their network, but the branding remains specific to the site/school/team they cover. Externally, every site is an independent brand with the awareness of the network umbrella brand an afterthought.

I think most fans like the site-specific names and branding, but that often leads to no connection or awareness about the parent company and the other communities under their umbrella.

But from the start, The Athletic has opted to have every site they launch incorporate the same uniform branding by just differing each site with adding the city’s name to it. New sites don’t require a new name, nor a new logo. They’re easier to launch, more recognizable to new readers and, more importantly, they are owned and operated by the parent company and thus their subscribers are much more secure than being tethered through an affiliate deal that could lapse.

While there are certainly pros and cons on the branding side, the simplicity of the uniform branding, as well as the ownership of the sites themselves, was something that obviously was not lost on investors as they started looking at the company’s long-term trajectory.

Buyers Market

The Athletic would be nowhere near where they are if not for the shaky ground underneath so many talented people within the industry. COO Adam Hansmann commented on this when I asked him what factors led to The Athletic significantly ramping up their ambitions.

“I would say more from a macro standpoint, kind of in the spring and early summer of 2017, what started to happen outside of our walls was ESPN going through a huge editorial downsizing, Fox Sports pivoting to video and, as you know, some of those scenarios freeing up talent like Stewart Mandel or Seth Davis or Ken Rosenthal.”

Whether it’s shrinking newsrooms at local newspapers or financial pressures of national networks combatting cable subscriber loss, The Athletic finds themselves flush with cash and in a buyer’s market, talent-wise. Awful Announcing has chronicled layoffs at pretty much all of the major national outlets and unfortunately, things aren’t much better at the local level.

Within the industry, there isn’t much confidence that more content jobs are going to be added and those that are will likely not be allocated towards reporting and long-form original writing. For some, a call from The Athletic is an new opportunity and adventure. For others, it’s viewed as a lifeboat.

What’s more than apparent to industry observers, and likely resonated with investors, is that The Athletic is in a favorable market for talent. With the business model already showing profitability in some cities, it’s easy to see why the investors would nudge The Athletic to put their foot down on the accelerator while the talent acquisition market conditions remained favorable and no competitor was lurking.

It’s easy to be skeptical about The Athletic, but you shouldn’t be

I get it. You’re skeptical. The majority of people who have reached out to me asking my opinion were more or less looking to confirm their skepticism.

While The Athletic is building up new sites, other more established brands are losing key personalities. The idea itself is so simple, and it just doesn’t make sense that traditional media companies wouldn’t have tried this. They’re growing too fast. It’s not sustainable. The content isn’t THAT good. People won’t pay for content they can find for free elsewhere. It’s a cult.

There is potentially some merit in some of those objections.

The Athletic is not a company trying to shoot for the moon by being a new social network or search engine. Because of the simplicity of the business model, I can tell you it’s not the type of business which would dazzle investors and compel them to write a huge check hoping for a multi-billion dollar outcome that would warrant such a risky investment.

They think they can make money by getting people to pay for sports content. It sounds way too simplistic and non-original to be worth hundreds of millions of dollars. Like your friend trying to get you into cryptocurrency and thinly veiled pyramid schemes before that, you just don’t buy it.

But whatever your intuition is telling you, I think the reality is that as simple and overly ambitious as The Athletic seems, the performance of the company has turned investors’ heads. And that has only thrown more fuel on the fire. While many things can and will go wrong at any startup, it’s hard for me to see The Athletic coming back to earth anytime soon — let alone going belly-up, like I’ve seen many predict.

It’s easy to dismiss or, in some cases, root against The Athletic for a variety of reasons. I’d argue that same type of systemic industry pessimism and skepticism have created the market conditions which have allowed The Athletic to go from a humble media startup trying to prove its business merit to the juggernaut that is now reinvigorating a stagnant industry.

The last sports media Cinderella birthed by Silicon Valley was built on SEO-juiced, clickbaity slideshows authored by unpaid writers. As much as I’d love to apply my own cynicism towards The Athletic, I’m hard-pressed to root against a company investing in quality content and allowing readers — not advertisers nor social networks and search engines — dictate their success. With that, I hope to avoid another 100 inquiries about The Athletic in the year to come.

** Please check out Awful Announcing’s interview with The Athletic COO Adam Hansmann about what’s next for the company.